Express News Today

Express News Today of market intelligence, Express News Today as an enterprising research and consulting company, believes in providing thorough landscape analyses on the ever-changing market scenario, to empower companies to make informed decisions and base their business strategies with astuteness.

What Are Key Trends in Computed Tomography Market?

The rising prevalence of chronic diseases and continuous developments in technology will be responsible for the significant growth in the computed tomography (CT) market in the years to come. A CT scanner fires conventional X-ray beams into the patient’s body from different angles and then uses a computer to present a cross-sectional view of the interior anatomy, by combining all the images. Today, CT is being widely used for seeing tissues, bones, nerves, blood vessels, and organs for tumors, clots, bleeds, inflammation, and tissue injury.

Computed Tomography Market - Global Opportunity & Industry Forecast Report

Every year, 17.9 million people die of heart diseases and 9.6 million of cancer, says the World Health Organization (WHO). The key to treating these and other chronic diseases is effective diagnosis, and this awareness has led to numerous advancements in the medical technology. For the most part of the 20th century, doctors relied on blood tests and conventional X-ray for disease diagnosis, but the results were not always reliable. In 1972, the advent of the CT technology forever changed the world of medical imaging.

The computed tomography market is growing due to the surging prevalence of chronic diseases, which is itself a result of many factors, such as overexposure to ultraviolet (UV) rays and pollution, poor lifestyle choices, such as smoking, fatty diet, drinking, and drug use, and genetic factors. Another factor that greatly increases the risk of contracting a disease of any kind is age. The elderly are physically and immunologically weak, which is why they fall sick quite a lot. With the geriatric population expected to touch 1.5 billion by 2050 by the United Nations, the volume of CT scans is set to boom massively.

Presently, North America is the largest contributor to the computed tomography market, majorly because of the high prevalence of chronic diseases. Six in 10 people in the U.S. have at least one chronic disease, says the Centers for Disease Control and Prevention (CDC). Additionally, chronic diseases are the leading contributor to the region’s mortality and morbidity burden, and they are also responsible for the increasing healthcare spending here. Moreover, the continent has an advanced healthcare infrastructure, which has resulted in the availability of highly efficient CT scanners.

Therefore, with more people suffering from chronic diseases, the demand for CT systems at hospitals and diagnostic centers will keep increasing.

Technological Advancements to Drive Interventional Radiology Market Growth

Due to the increasing incidence of chronic diseases, surging demand for minimally invasive procedures, rising elderly population, and technological advancements, the interventional radiology market is projected to demonstrate a CAGR of 6.4% during the forecast period (2019–2024). The market generated $19.0 billion revenue in 2018, which is expected to reach $27.3 billion by 2024. This market is also led by strategic measures, such as product launches and marketing approvals.

Access Report Summary - Interventional Radiology Market Growth

Increasing prevalence of chronic diseases, such as cancer and cardiovascular diseases (CVDs), is expected to have a positive impact on the interventional radiology market. Moreover, the rising number of interventional cardiology procedures, including percutaneous coronary interventions (PCI), transcatheter aortic valve implantations (TAVI), and transcatheter aortic valve replacement (TAVR), supplements the demand for interventional radiology systems to treat CVDs.

Further, the interventional radiology market growth is driven by the technological developments in the interventional procedures applied for treating several chronic diseases. These developments have led to the introduction of various advanced products that help in early diagnosis of several diseases, which assists in timely management of these diseases. One such product is GE Healthcare's image-guided system (IGS) that is used in complex procedures, such as chronic total occlusion in blood vessels and structural heart, due to its enhanced visualization.

Globally, the North American interventional radiology market accounted for the largest share in 2018, due to the improved healthcare infrastructure and high healthcare expenditure. On the other hand, during the forecast period, the Asia-Pacific (APAC) market is projected to display the fastest growth, owing to the increasing incidence of chronic diseases, improving healthcare system, surging geriatric population, and rising healthcare spending. Additionally, increasing frequency of scientific meetings and training programs to develop interventional radiology is expected to boost the market growth in the region, during the forecast period.

Safety Lancets Minimize Risk of Accidental Pricks

The rising cases of chronic obstructive pulmonary diseases (COPDs), diabetes, cancer, and cardiovascular diseases (CVDs) have amplified the adoption of minimally invasive blood-drawing devices such as lancets. According to the World Health Organization (WHO), currently nearly 235 million people are suffering from asthma and around 3 million individuals die due to COPDs each year. The organization also states that cancer kills around 9.6 million people and heart diseases claim 17.9 million human lives each year. Medical professionals use lancets to diagnose such diseases at their early stages to reduce the mortality rate.

Access Detailed Report - Lancet Market Revenue Estimation

Additionally, the escalating adoption of such medical devices in homecare settings will fuel the lancet market at a CAGR of 9.5% during the forecast period (2020–2030). The market generated $830.3 million revenue in 2019. Lancets made for homecare settings are easier to utilize than those applied in hospitals and clinics. Owing to their easy availability and usage, the devices are gaining wide popularity among the geriatric population, especially among diabetic patients.

In recent years, major market players have started entering into distribution agreements with smaller firms to magnify their sales in regions beyond their direct sales channels' reach. For instance, Owen Mumford Ltd. signed an agreement with NIPRO Corporation, in July 2019. The former aims to increase the distribution channel of UniSafe springless devices in Japan through the latter, which is an Osaka-based firm. Other players following the same footprint include F. Hoffmann-La Roche Ltd., B. Braun Melsungen AG, and HTL-STREFA S.A.

According to P&S Intelligence, North America adopted the highest number of lancets in 2019, due to the rising prevalence of chronic diseases, surging population of elderly people, and increasing technological advancements, in the region. According to the Center for Disease Control and Prevention (CDC), in the U.S., more than 34 million individuals are living with diabetes. The CDC also states that nearly 600,000 deaths in the country occur due to cancer and approximately 1.7 million cases are registered every year.

Whereas, the Asia-Pacific lancet market will exhibit the fastest growth during the forecast period. This can be ascribed to the improving healthcare infrastructure, booming elderly population, magnifying purchasing power, rising prevalence of chronic ailments, and increasing number of initiatives by public and private organizations to spread awareness regarding diabetes. The United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP) propounds that by 2050, one in four people in the region will be over 60 years old. Further, the WHO states that around 6 million people in Southeast Asia have diabetes.

Thus, the increasing preference for minimally invasive procedures and the booming number of diabetic patients will propel the usage of lancets in the coming years.

Governments Raising Awareness About Chronic Pain Treatment Solutions

Governments across the world are making efforts to raise awareness regarding advanced pain treatment products and services to enhance healthcare system. For example, the International Association for the Study of Pain (IASP) executed its Developing Countries Project from January 2018 to March 2018, to impart pain education and encourage chronic pain treatment services in developing nations, by providing grants. These grants aspire to enhance the availability and scope of essential educations for clinicians engaged in pain treatment, to inspire the development of innovative approaches.

Browse detailed report - Chronic Pain Treatment Market Revenue Estimation and Growth Forecast

Besides, the surging geriatric population and accelerating cases of chronic illnesses will fuel the chronic pain treatment market at 6.5% CAGR during 2020–2030. The market generated $77.8 billion in 2019 and it is projected to reach $151.7 billion by 2030. Chronic ailments like neurological disorders, cancer, and orthopedic diseases lead to long-lasting pain that require multiple pain management options. Additionally, the surging incidence of joint pain, lower pack pain, neck pain, and migraine have accelerated the demand for pain treatment services like psychological therapy, neuroablation, and physiotherapy, globally.

The aforementioned trend in the chronic pain treatment market has led to the introduction of products like Voltaren Arthritis Pain gel and Proclaim XR SCS system by GlaxoSmithKline plc and Abbott Laboratories, respectively. GlaxoSmithKline plc received approval for this product from the Food and Drug Administration (FDA) in February 2020. Voltaren Arthritis Pain gel is designed for patients aged 18 years and above to offer temporary relief from arthritis pain, and it is the first prescription-based nonsteroidal anti-inflammatory drug (NSAID), which is available over the counter (OTC) in the U.S.

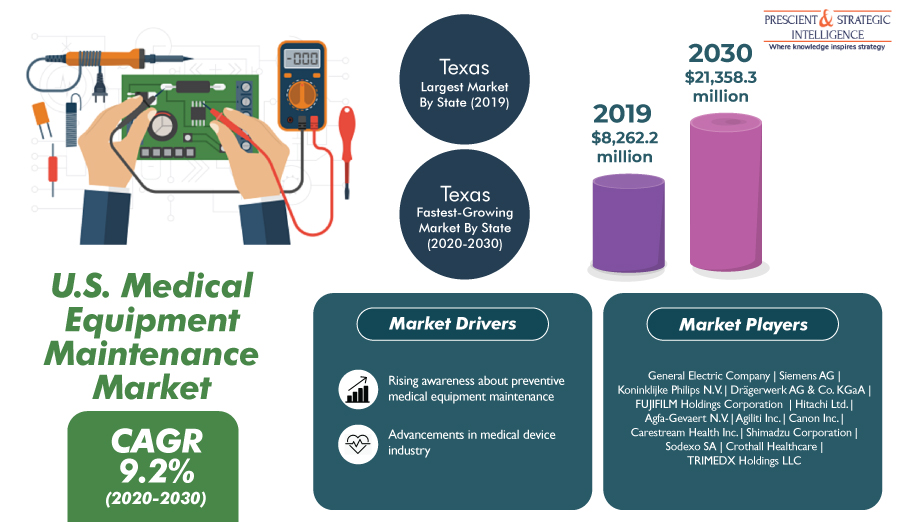

Why Are OEMs Preferred Medical Equipment Maintenance Service Providers in U.S.?

At $11,072, the per capita healthcare expenditure of the U.S. was the highest in the world in 2019, as per the Organisation for Economic Co-operation and Development (OECD). The expenditure includes all the spending on constructing healthcare centers, procuring equipment, and hiring staff, as well as offering medical services in the form of diagnosis, treatments, and medicines. Apart from this, a significant portion of the spending is done for the regular maintenance of medical equipment in the country.

Browse detailed report with COVID-19 impact analysis at U.S. Medical Equipment Maintenance Market Research Report

This is necessary as medical devices are used on numerous patients throughout the day and the larger pieces of equipment work almost nonstop. Being however advanced as they are, they are still machines, thus are prone to malfunctioning. As a result of all these factors, the U.S. medical equipment maintenance market revenue, which stood at $8,262.2 million in 2019, will increase to $21,358.3 million by 2030, at a 9.2% CAGR between 2020 and 2030.

And, it is not just the rising awareness of the healthcare fraternity on such issues that is driving medical equipment maintenance activities in the country but also the stringent regulations of the government. The Joint Commission (TJC), Det Norske Veritas (DNV), Healthcare Facilities Accreditation Program (HFAP), United States Food and Drug Administration (USFDA), state departments of health, and Centers for Medicare and Medicaid Services (CMS) mandate compliance with medical equipment maintenance guidelines.

As per P&S Intelligence, the largest contributor to the U.S. medical equipment maintenance market is Texas, on account of the large number of medical centers here and its high healthcare spending. Since over 80% of its healthcare spending is done by the Texas Department of Aging and Disability Services (DADS), Texas Health and Human Services Commission (HHSC), Texas Department of State Health Services (DSHS), Teacher Retirement System (TRS), and Employees Retirement System (ERS), hospitals and other facilities here can easily afford the expensive medical equipment maintenance services.

Hence, with the growing awareness on the preventive maintenance of medical devices and the stringent U.S. government rules in this regard, OEMs and ISOs are expected to win more service contracts in the coming years.

us medical equipment maintenance market

us medical equipment maintenance market size

us medical equipment maintenance market share

us medical equipment maintenance market demand

us medical equipment maintenance market growth

us medical equipment maintenance market outlook

us medical equipment maintenance market trends

us medical equipment maintenance market

us medical equipment maintenance market size

us medical equipment maintenance market share

us medical equipment maintenance market demand

us medical equipment maintenance market growth

us medical equipment maintenance market outlook

us medical equipment maintenance market trends

Why will North American Defibrillators Market Exhibit Rapid Progress in U.S in Coming Years?

Driven by the soaring geriatric population, increasing prevalence of cardiac disorders, ballooning requirement of automated external defibrillators (AEDs), and rapid developments and innovations in defibrillation technology, the North American defibrillators market is predicted to grow, in valuation, from $6.1 billion to $8.1 billion from 2017 to 2023. Furthermore, as per the predictions of P&S Intelligence, a market research firm based in India, the market will exhibit a CAGR of 4.9% from 2018 to 2023.

Browse report overview and detailed TOC at North American Defibrillators Market Demand Forecast

The surging geriatric population in many North American countries is one of the major factors responsible for the growth of the North American defibrillators market. In North America, the population of geriatric people is growing at the fastest rate in the U.S. As per the report published by the Population Reference Bureau in 2018, the total number of people in the age bracket (65 years and above) in the U.S. is predicted to rise from 46 million to more than 98 million during 2014—2060.

Public access settings, hospitals, clinics, and cardiac centers, home care settings, and pre-hospital care settings are the main categories present under the end user segmentation of the market. Out of these categories, the hospitals, clinics, and cardiac centers category generated the highest revenue in the market over the last few years. However, the fastest market growth will be exhibited by the public access settings category in the future years, owing to the ballooning utilization of AEDs in this category.

Public access settings, hospitals, clinics, and cardiac centers, home care settings, and pre-hospital care settings are the main categories present under the end user segmentation of the market. Out of these categories, the hospitals, clinics, and cardiac centers category generated the highest revenue in the market over the last few years. However, the fastest market growth will be exhibited by the public access settings category in the future years, owing to the ballooning utilization of AEDs in this category.

The North American defibrillators market is also expected to exhibit rapid growth in Canada over the next few years. This is primarily attributed to the rising government incentives and measures being taken in the country, such as investments and other initiatives, for increasing awareness and providing defibrillation training to the people, increasing incidence of cases of sudden cardiac arrests, and the existence of several local defibrillators supplying companies in the country.

Defibrillators Offering Heart Patients New Lease of Life

The growth of the defibrillator market is driven by several key factors, such as the rising incidence of cardiac diseases, increasing improvements in the defibrillation technology, booming population of the elderly, and surging strategic development activities among major players. These factors will propel the market at a CAGR of 7.2% during the forecast period (2020–2030). The market generated $9,621.2 million in 2019, and it is expected to reach $20,281.6 million by 2030.

Browse detailed report on Defibrillator Market - Global Industry Analysis and Growth Forecast to 2030

Hospitals, clinics, and cardiac centers are the largest users of defibrillators, as they regularly adopt advanced medical equipment that offers higher efficiency, for a lower death rate. Apart from this, defibrillators of various types are available at public-access settings, pre-hospital care settings, and homecare settings. The different types of defibrillators include implantable cardioverter defibrillators (ICDs), such as transvenous ICDs (T-ICDs) and subcutaneous ICDs (S-ICDs), and external defibrillators, including manual and automated ones (AEDs).

Geographically, the North American defibrillator market generated the highest revenue in the historical period (2014–2019), and it is expected to witness lucrative growth in the forecast period. This can be ascribed to the heavy investments by public and private organizations to amplify research and development (R&D) regarding the defibrillation technology, strong presence of key market players, favorable reimbursement policies, and well-developed healthcare sector. Due to these factors, patients in the region can easily afford the expensive medical care that includes the use of ICDs and other defibrillators.

Thus, the increasing prevalence of CVDs, developing healthcare infrastructure, and rising R&D on the defibrillation technology will augment the demand for these medical devices in the coming years.

Thus, the increasing prevalence of CVDs, developing healthcare infrastructure, and rising R&D on the defibrillation technology will augment the demand for these medical devices in the coming years.

How is Rising Number of Data Breaches Driving Demand for Blockchain in Healthcare?

As per a P&S Intelligence report, the global blockchain in healthcare market is predicted to reach a value of $890.5 million by 2023, from $44.6 million in 2017, and is expected to advance at a 67.1% CAGR during the forecast period (2018–2023). The market is growing due to the increasing investments and funding in the blockchain technology, rising number of regulations for safeguarding consumer data, and implementation of blockchain in pharmaceutical supply chain.

Access Report Summary - Blockchain in Healthcare Market Segmentation Analysis

On the basis of application, the market is divided into prescription drug abuse, drug discovery and clinical trials, drug supply chain management, claims adjunction and billing management, clinical data exchange and interoperability, and others. Out of these, the clinical data exchange and interoperability application held the major share of 40.0% of the market in 2017, due to the fact that the blockchain technology can transform the way clinical information and data are stored and shared across the total care continuum, such as patients, payers, and healthcare partners.

Geographically, the blockchain in healthcare market was dominated by North America in 2017, however, the European region is projected to emerge as the largest market by 2023. The major reasons for this is the implementation of various blockchain initiatives by private and public sector players in the region. The Asia-Pacific region is expected to progress at the fastest pace during the forecast period, which can be ascribed to the increasing focus on the blockchain technology in the region for catering to the unmet needs in areas of drug supply chain management and clinical data exchange and interoperability.

The blockchain technology is still in the nascent stage, owing to which companies that are interested in adopting the technology are collaborating and partnering with several technology providers for exploring its potential applications. For example, a deal between NMC Health, a United Arab Emirates (UAE) based private sector healthcare provider, and Guardtime AS, an Estonian blockchain pioneer, was finalized in January 2018 for introducing the technology in the country.

In conclusion, the market is being driven by the rising implementation of regulations for safeguarding consumer data and rising number of collaborations and partnerships.

Hospitals Deploying Radiotherapy Equipment to Treat Cancer

According to the Global Cancer Observatory (GLOBOCAN), 2020 saw a total of 19.3 million cancer cases and 10 million cancer deaths worldwide. The International Agency for Research on Cancer (IARC) states that globally, 1 in 5 people are affected by cancer during their lifetime, and 1 in 11 women and 1 in 8 men die of it. As per research, socio-economic factors and aging are the prime causes of cancer. Owing to this reason, the usage of radiotherapy is expected to increase in the coming years.

Receive Sample Copy of this Report: https://www.psmarketresearch.com/market-analysis/radiotherapy-market-revenue/report-sample

Additionally, technological advancements in radiation therapy are projected to accelerate the radiotherapy market at a CAGR of 8.4% during the forecast period (2020–2030). For instance, automated products are being incorporated into clinical practice systems to enhance the treatment process. Moreover, the advent of more-precise forms of radiotherapy treatment, such as volumetric modulated arc therapy (VMAT), proton therapy, stereotactic radiosurgery (SRS), brachytherapy, and image-guided radiation therapy (IGRT), will help the market revenue increase from $7,222.4 million in 2019 to $17,194.4 million by 2030.

Make an Enquiry before Purchase: https://www.psmarketresearch.com/send-enquiry?enquiry-url=radiotherapy-market-revenue

Radiotherapy is primarily used in hospitals as they are the initial point of contact for the diagnosis and treatment of diseases. These healthcare facilities offer the best-possible services due to the presence of trained healthcare professionals and technologically advanced medical devices. Moreover, the increasing cases of cancer, booming geriatric population, and growing healthcare expenditure will lead to the largescale adoption of radiotherapy devices in hospitals. In addition to hospitals, cancer research institutes and independent radiotherapy centers deploy radiotherapy devices to develop new technologies and diagnose tumors, respectively.

At-Home Drug of Abuse Testing Market to Witness Robust Growth in Coming Years

Factors like increasing use of illicit drugs among teenagers; growing production of bath salts, synthetic cannabinoids, and other emerging drugs; and rising number of government initiatives to reduce the levels of drug abuse are projected to increase the at-home drug of abuse testing market size from $483.6 million in 2017 to $831.9 million by 2023.

One of the prime factors driving the at-home DOA testing market growth is the increasing abuse of illicit drugs by teenagers. Adolescents, these days, are trying and experimenting with several illicit substances, such as drugs and alcohol, to escape from their troubles. In this search for an escape route, teenagers use drugs and gradually become addicted to them. To keep a check on these young kids, educational institutions and parents are adopting at-home drug of abuse (DOA) products like dip cards and strips.

Receive Sample Copy of this Report: https://www.psmarketresearch.com/market-analysis/at-home-doa-testing-market/report-sample

The product segment under the at-home drug of abuse testing market is bifurcated into rapid DOA test kits and breath analyzers. The rapid DOA test kits category is further classified into test dip cards, test strips, test cups, and others. During the forecast period, the rapid DOA test kits category is projected to display faster growth than the breath analyzers. This can be ascribed to the surging adoption of rapid DOA test kits like dip cards and test cups because of their lower costs.

Additionally, the sample segment of the at-home DOA testing market is categorized into urine, saliva, hair, and others. Amongst these, the urine category dominated the market during the historical period, and is expected to display the fastest growth during the forecast period. This is attributed to the large-scale application of urine drug testing products, as they are easy to use and available at a low cost.

Rising Cases of Chronic Wounds Boosting LATAM Wound Dressing Market

Factors such as the rising prevalence of diabetes, growing aging population, increasing cases of injuries and physical trauma, and surging incidence of chronic wounds are projected to propel the growth of the Latin American (LATAM) wound dressing market at a CAGR of 5.0% in the forecast period (2021–2030). At this growth rate, the market size is expected to reach $549.5 million by 2030 from $344.3 million in 2020. Moreover, the market is witnessing a shifting preference toward more-advanced products from traditional wound dressings.

Receive Sample Copy of this Report: https://www.psmarketresearch.com/market-analysis/latam-wound-dressing-market/report-sample

Moreover, the surging incidence of chronic wounds is another key factor driving the LATAM wound dressing market. The burden of chronic illnesses like cancer and cardiovascular diseases is growing rapidly in LATAM. For example, as per the International Agency for Research on Cancer (IARC), in 2020, the number of new cancer cases reached 1.4 million and 713,414 cancer-related deaths were reported in the region. Cardiovascular disorders and cancer often lead to chronic wounds, which are tough to heal and need extensive care for a longer period of time.

Make an Enquiry before Purchase: https://www.psmarketresearch.com/send-enquiry?enquiry-url=latam-wound-dressing-market

The type segment of the LATAM wound dressing market is classified into advanced and traditional. Of these, the advanced category accounted for the larger market share in 2020, and it is projected to witness the faster growth in the coming years. This can be ascribed to the surging incidence of chronic wounds, along with the rising cases of chronic diseases and the increasing usage of advanced dressing products for the treatment of these wounds, in the LATAM region.

Growing Adoption of Targeted Therapy Driving Immunotherapy Drugs Market

In 2017, the global immunotherapy drugs market reached a value of $106.1 billion and is predicted to advance at a 13.6% CAGR during the forecast period (2018–2023). The market is growing because of the rising availability of biosimilars, surging prevalence of chronic diseases, increasing implementation of target therapy, and rising demand and development of mAbs. Immunotherapy is the treatment of a disease by enhancing, inducing, or suppressing an immune response for fighting against infection and disease. In terms of type, the immunotherapy drugs market is bifurcated into vaccines and checkpoint inhibitors.

Receive Sample Copy of this Report:https://www.psmarketresearch.com/market-analysis/immunotherapy-drugs-market/report-sample

When therapy area is taken into consideration, the immunotherapy drugs market is categorized into infectious diseases, cancer, and autoimmune and inflammatory diseases. Out of these, the cancer category accounted for the major share of the market during the historical period and is projected to contribute the largest revenue share to the market during the forecast period as well, owing to the rising prevalence of cancer across the world. The autoimmune & inflammatory diseases category is predicted to grow at the fastest pace during the forecast period.

Make an Enquiry before Purchase:https://www.psmarketresearch.com/send-enquiry?enquiry-url=immunotherapy-drugs-market

The rise in prevalence of chronic diseases, including rheumatoid arthritis, cancer, autoimmune diseases, and diabetes, is a major driving factor of the immunotherapy drugs market. For example, according to the World Health Organization, in 2018, cancer caused about 9.6 million deaths. The management of these diseases need therapeutic intervention and immunotherapy drugs help in mitigating the impact of these diseases. In addition, various drugs manufactured by the players operating in the market for the treatment of chronic diseases are under clinical trials. These factors are resulting in the growth of the market.

Out of all the regions, North America held the largest share of the immunotherapy drugs market during the historical period and is projected to retain its position during the forecast period. The reasons for this are the increasing prevalence of chronic diseases, rising per capita healthcare spending, growing geriatric population, and presence of major players in the region. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period. This is ascribed to the rising number of research & development activities which are being conducted in the region.

Hence, the market is being driven by the increase in the implementation of target therapy and rising prevalence of chronic diseases.

Pulse and Regional Oximeters Market to Witness Robust Growth in Coming Years

The global pulse and regional oximeters market reached a value of $2,101.0 million in 2018 and is expected to attain a value of $3,365.0 million in 2024, advancing at an 8.2% CAGR during the forecast period (2019–2024).

The market is growing due to the supportive government initiatives, increasing number of patent approvals and commercialized products, rising number of medication errors, and surging incidence of targeted diseases. Electronic devices which measure oxygen saturation level in red blood cells is called a pulse oximeter. A regional oximeter measures regional hemoglobin oxygen saturation.

Receive Sample Copy of this Report:https://www.psmarketresearch.com/market-analysis/pulse-and-regional-oximeters-market/report-sample

When product type is taken into consideration, the pulse and regional oximeters market is categorized into nose, fingertip, palm/foot, table-top, forehead, wrist-worn, earlobe, and handheld. Among these, the fingertip category held the largest share of the pulse oximeter market during the historical period (2014–2018) and is projected to dominate the market during the forecast period as well. This is because fingertip pulse oximeters are widely used in different applications and are portable. The fastest growth is predicted to be witnessed by the wrist-worn category during the forecast period.

Make an Enquiry before Purchase:https://www.psmarketresearch.com/send-enquiry?enquiry-url=pulse-and-regional-oximeters-market

Another major driving factor of the pulse and regional oximeters market is the surging incidence of targeted diseases. The requirement for these devices is rising due to the different types of patients that are being admitted in different healthcare settings. Pulse and regional oximeters are required for patients suffering from different diseases, such as drowning condition, cardiac arrest, apneic conditions, multisystem trauma, and sickle-cell crises. These devices have emerged as useful devices for the evaluation of patient’s oxygenation status and are widely utilized in several departments or units of healthcare settings.

Thus, the market is growing considerably because of the rising incidence of targeted diseases and surging number of medication errors.

What are Reasons behind Growth of Lip Cold Sore Treatment Market?

In China and Southeast Asia (SEA), the prevalence of herpes simplex virus type-1 (HSV-1) infection is increasing. Mostly transmitted via mouth–mouth contact, the infection often presents with no symptoms, which makes infected people a potential carrier without their knowledge. This is the reason the China and SEA lip cold sore treatment market size is set to increase to $85,265.1 thousand in 2030 from $45,262.1 thousand in 2020, at a 6.7% CAGR between 2021 and 2030.

HSV-1 infection most commonly presents on and around the lips as blisters. The most-prominent symptoms of this infection are painful gums, headache, fever, swollen lymph nodes, muscle ache, and sore throat. Apart from being in contact with infected people, fatigue, abnormal hormone levels, physical trauma, physiological and psychological stress, and immunosuppression greatly elevate the risk of HSV-1. Thus, the China and SEA lip cold sore treatment market is growing with the rising demand for products that can offer symptomatic relief and speed up the healing of the sores.

Get the Sample Copy of this Report at @ https://www.psmarketresearch.com/market-analysis/lip-cold-sore-treatment-market/report-sample

The containment measures taken in the wake of the COVID-19 pandemic have led to the shutting down of factories and reduced trade of an array of products. As a result, the China and SEA lip cold sore treatment market was negatively affected due to the curtailed manufacturing activities and people staying home. Moreover, the widespread financial distress has forced people to spend only on essential stuff, such as important medication and ration.

The SEA lip cold sore treatment market has been the most productive in China till now, and this country is also set to witness the highest CAGR in the years to come. With the increasing prevalence of HSV-1 infection in rural China and the increasing awareness on this disease, the demand for the related treatment products is rising in the country.

Make enquiry about this report at @ https://www.psmarketresearch.com/send-enquiry?enquiry-url=lip-cold-sore-treatment-market

The most-significant players in the China and SEA lip cold sore treatment market include Perrigo Company plc, Kyungdong Pharmaceutical Co. Ltd., Church & Dwight Co. Inc., Quantum Health, Integria Healthcare (Australia) Pty. Ltd., Carma Labs Inc., Blistex Inc., Li & Fung Limited, Alliance Pharma plc, Viatris Inc., URGO Group, GlaxoSmithKline plc, and Laboratoire HRA Pharma SAS.

Immunotherapy Drugs Market Industry Analysis, Size, Trends and Future Scope

The key driver of this market is an increase in the prevalence of chronic diseases and thriving demand and development of monoclonal antibodies (mAbs) and immunotherapy drugs. Immunotherapy refers to the treatment of a disease by enhancing, inducing, or suppressing an immune response.

Across the globe, the increasing prevalence of chronic diseases has become a major healthcare burden, as it affects people in high-income as well as low and middle-income countries (LMIC). According to a World Health Organization report, the fact that cancer led to an estimated 9.6 million deaths in 2018 firmly cements this claim. The organization further reported that around 70% of all deaths from cancer occur in LMICs.

Download Report Sample at:https://www.psmarketresearch.com/market-analysis/immunotherapy-drugs-market/report-sample

Furthermore, in a report of the International Agency for Research on Cancer (IARC) in 2018, it is estimated that around 18.1 million people were suffering from cancer globally, and the number is projected to reach 29.5 million by 2040. Similarly, a study conducted between 2005 and 2015 by the American Medical Association found that cancer cases increased by 33% during this period, of which 16.4% cases were due to aging population. Hence, the growing use of immunotherapy drugs to meet the increasing prevalence of chronic diseases in the elderly is driving the immunotherapy drugs market.

That same month, Allogene Therapeutics Inc. and Pfizer Inc. signed an asset contribution agreement to use Pfizer’s allogeneic CAR-T therapy, which is investigational immune cell therapy, for cancer. This agreement provided an opportunity for Pfizer Inc. to continue the development of the CAR-T therapy. Other players operating in the global immunotherapy drugs market, such as AstraZeneca PLC, F. Hoffmann-La Roche Ltd., Eli Lilly and Company, Sanofi, Medigene AG, AbbVie Inc, Johnson & Johnson, Amgen Inc., Merck & Co. Inc., GlaxoSmithKline plc, C. H. Boehringer Sohn AG & Co. KG, Novartis International AG, Takeda Pharmaceutical Company Limited, and Celgene Corporation, are taking similar steps.

Hence, as more people get affected by chronic diseases in the future, the immunotherapy drugs sector will continue to prosper.

Human Insulin Market Share Analysis of the Top Industry Players, Growth Opportunities and Country Level Segments

On account of the growing number of diabetic patients, increasing geriatric population, technological advancements in insulin delivery devices, and rising population exposed to risk factors are leading to the growth of the human insulin market. The global market generated a revenue of $42.9 billion in 2017, and it is expected to witness a CAGR of 8.8% during the forecast period (2018–2023). Human insulin (HI) is synthetic insulin, which mimics the effects and functionality of natural insulin in humans. It is generally created by growing the insulin protein in the E. coli bacteria.

In a recent P&S Intelligence research, the human insulin market is segmented by type, application, and region. Under the product segment, the market is further divided into HI drugs and delivery devices. Due to increase in research and development activities for drugs discovery and manufacture, and high prevalence of diabetes, HI drugs held the larger share (79.5%) in the market in 2017 in terms of value. Furthermore, the rise in geriatric population and growth in demand for HI analogs is also pushing the market progress; analogs and biologics are two categories of the HI drugs division.

Download Sample of This Research Report:

https://www.psmarketresearch.com/market-analysis/human-insulin-market/report-sample

Similarly, the application segment of the human insulin market consists of type 1 diabetes, type 2 diabetes, and gestational diabetics and prediabetes categories. Type 2 diabetes states a progressive condition, in which the body becomes resistant to the effects of insulin or gradually fails to produce adequate insulin in the pancreas. In 2017, HI drugs and delivery devices for type 2 diabetes held the largest share in the sector, registering a revenue of $35.1 billion. This was because the prevalence of type 2 diabetes is increasing across the globe with the passing of each day.

Therefore, it is apparent that the steady growth of the market will give players lucrative opportunities to invest in the research and development of improved insulin drugs and delivery systems.